The coming weeks will likely prove turbulent in economic terms. The ECB, the Federal Reserve, the Bank of England, and the Bank of Japan, have all unveiled plans to further loosen monetary policy more or less simultaneously. Central banks in these economies are trying their best to find a way to unleash economic growth by easing credit conditions. These central banks are now resolutely focused on the short-run. What all this loosening portends for the medium to long-term is anyone’s guess. In this post, and some to come, I want to devote attention to implications for Canada.

The plot below shows the policy rates set by the Bank of Canada and the Federal Reserve Board from 2008–August 2012. The US policy rate has been near the zero lower bound (ZLB) since 2008 and, if the expectations of the members of the FOMC are to be believed, following their September 2012 meeting, the straight line near zero will likely extend into 2015. In the meantime, other than in 2009 —when Canada’s overnight rate spent some time at the Canadian equivalent of the ZLB (i.e., 25 bp) — the Bank of Canada’s policy rate (the overnight rate) has also remained at 1% since September 2010, that is, for over 2 years.

NOTE: the fed funds rate is actually a range (0–0.25%) but in the above figure the rounded mid-point of the range is used (0.13%). Also, the Fed and the Bank of Canada both meet 8 times a year while the above data have been averaged to create a monthly series.

The next figure plots the yield on long-term government bonds, again for the US and Canada. Although the Bank of Canada has not yet had to engage in the kind of the quantitative easing or credit easing policies engineered by the Fed, the two yields move more or less in tandem. The spread between the two yields does, however, change and this is likely indicative of the relatively better economic environment that Canada has experienced before and since the financial crisis erupted in the US in 2007.

Source: International Monetary Fund, International Financial Statistics CD-ROM, August 2012.

Nevertheless, it is also clear that US monetary policy, from QE1 through QE3, is also helping to drag down interest rates in Canada. Recent research by economists at the St. Louis Fed suggests that "unorthodox" US monetary policy is indeed influencing Canadian interest rates while there are growing indications that the Swiss National Bank’s determination to put a floor on its exchange rate against the euro may also be having repercussions on spreads between Swiss and euro area member sovereign debt (e.g., see this FT column).

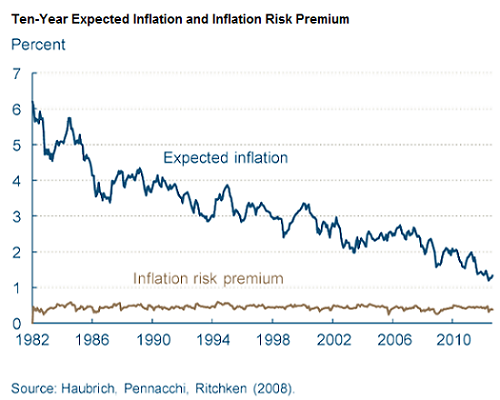

Also helping matters is the remarkable anchoring of inflation expectations. Some are even referring to a virtual "cementing" of inflationary expectations. The figure below, for the US and based on financial market data, shows not only the decline of inflation expectations since the early 1980s but that the inflation risk premium, which might have been positively affected by successive bouts of QE, has barely budged.

Source: Cleveland Federal Reserve, http://www.clevelandfed.org/research/data/inflation_expectations/.

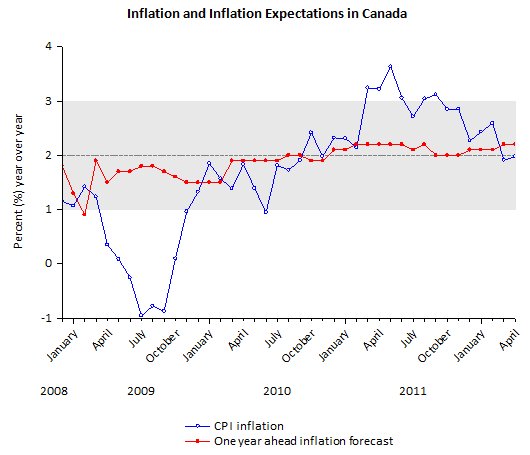

Canada, of course, has an inflation target of 2% with a tolerance range of 1–3%. Headline CPI inflation has varied considerably, undershooting the lower bound of the range during the height of the global financial crisis. Until recently, CPI inflation has been overshooting the target. Indeed, since April of this year, the Bank of Canada has been using the press release that accompanies the policy rate decision to announce that “some modest withdrawal” of what it deems to be “considerable monetary stimulus” may become necessary.

An optimistic view of how monetary policy behaves suggests that the Bank’s "moral suasion" has worked wonders although markets will no doubt begin to ask at some point whether the Bank is "all talk, no action" if it keeps delaying the threatened interest rate increase. Equally difficult is how the Bank explains why it plans to possibly raise the policy rate when other central banks have been latterly lowering theirs (more on this below).

Sources: Bank of Canada, International Monetary Fund, International Financial Statistics CD-ROM, August 2012, and The Economist Poll of Forecasters.The shaded area is the Bank of Canada inflation target range.